How Young Professionals Can Use Step-Up SIP Calculators To Beat Lifestyle Inflation

Look at your bank statement from two years ago. Then look at last month's. Income went up, sure. But so did everything else, and somehow the gap between what you earn and what you actually keep has barely moved. That is lifestyle inflation doing its quiet work. If you are running a flat SIP through this, you are losing ground without realising it. A step up sip calculator is one of the few tools that lets you see this problem in numbers before it becomes a regret, and most people in their twenties have not used one properly even once.

The Quiet Maths Nobody Warns You About

Lifestyle inflation is not the villain people imagine. It is not Goa trips or AirPods. It is the slow drift where a 20 percent hike turns into a 4 percent bump in savings and a 16 percent bump in everything else. Rent goes up because you wanted a balcony. Swiggy goes up because cooking feels exhausting after a 10-hour day. Subscriptions multiply.

None of it feels wrong in the moment. Each upgrade is justifiable on its own.

The problem shows up only when you zoom out. Your salary grows in a straight line. Your spending grows in a curve. And your savings rate, the one number that actually decides whether you retire at 55 or 70, quietly slides downwards while your CTC keeps rising.

Why a Flat SIP Stops Working

When you started that ₹10,000 SIP at 24, it was maybe 25 percent of your take-home. Three appraisals later, the same ₹10,000 is closer to 8 percent. You feel responsible because the SIP is still running. But it is doing a smaller share of the work every year, and inflation is chipping away at the rest.

Compounding does not care about your good intentions. It cares about how much you feed it.

How a Step Up SIP Calculator Actually Helps

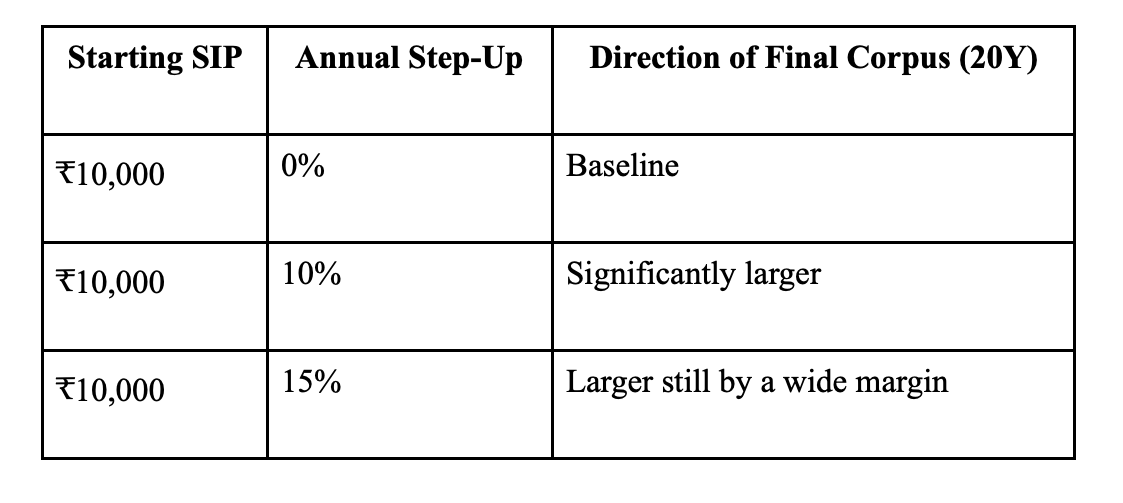

Here is what the tool does. You enter a starting SIP, an annual step-up percentage (most people pick somewhere between 10 and 15), an expected return, and a tenure. The calculator projects what your corpus looks like if you actually raise the SIP every year, not just on the day you got inspired.

A rough sense of what changes:

Numbers will move with the return assumption, of course. But the shape of the answer holds. A modest annual top-up does more for your final number than chasing one extra percent of return. You can play with your own combinations on the step up sip calculator and see this for yourself.

Using It Like You Mean It

Plugging numbers in once and feeling impressed is not the point. The calculator is useful only if it changes what you do in April, when your appraisal letter lands.

A few things that work in practice:

Pick a step-up percentage that sits below your average hike. If you usually get 12 to 14 percent, set the step-up at 10. That keeps some room for lifestyle improvements without letting them eat the whole increment.

Run the calculator twice. Once before your appraisal conversation, so you walk in knowing what the next number does to your 2045 self. Once after, to lock the new SIP amount the same week the salary hits.

Build separate projections for separate goals. Retirement, a flat in Bangalore, your kid's college. One blended number hides too much.

The trick is removing emotion from the loop. Decide the step-up in advance. Automate it. Stop revisiting the decision every month.

What the Calculator Will Not Tell You

A few honest caveats. The projection assumes you follow through every year, and life sometimes refuses to cooperate. A wedding, a job change with a gap month, a parent's hospital bill. Build a small cushion so one skipped year does not break the plan.

Also, the corpus number on screen is a planning estimate, not a contract. Equity returns are lumpy. You can get five flat years followed by a strong run, or the reverse. The calculator smooths all of that into an average, which is fine for planning and misleading if you treat it as a forecast.

And pick decent funds. A 15 percent step-up into a fund that consistently underperforms its category does worse than a 10 percent step-up into a steady one.

Conclusion

Most people in their late twenties think the next decade is about earning more. It is also about keeping more, and the two are not the same thing. A step up sip calculator gives you a way to make sure your investments grow at the speed your income grows, instead of staying frozen at whatever number felt brave when you started. Open one this weekend. Pick a percentage. Set the calendar reminder for April. Future you will not remember this Sunday, but they will remember the corpus.